A Smarter Way to Underwrite: Behavior Over Score

For too long, lenders have relied on traditional credit scores like FICO and Vantage to guide underwriting decisions. But these scores can lose meaning in the lower bands — often missing the real story behind how someone manages their money. It’s time to go deeper.

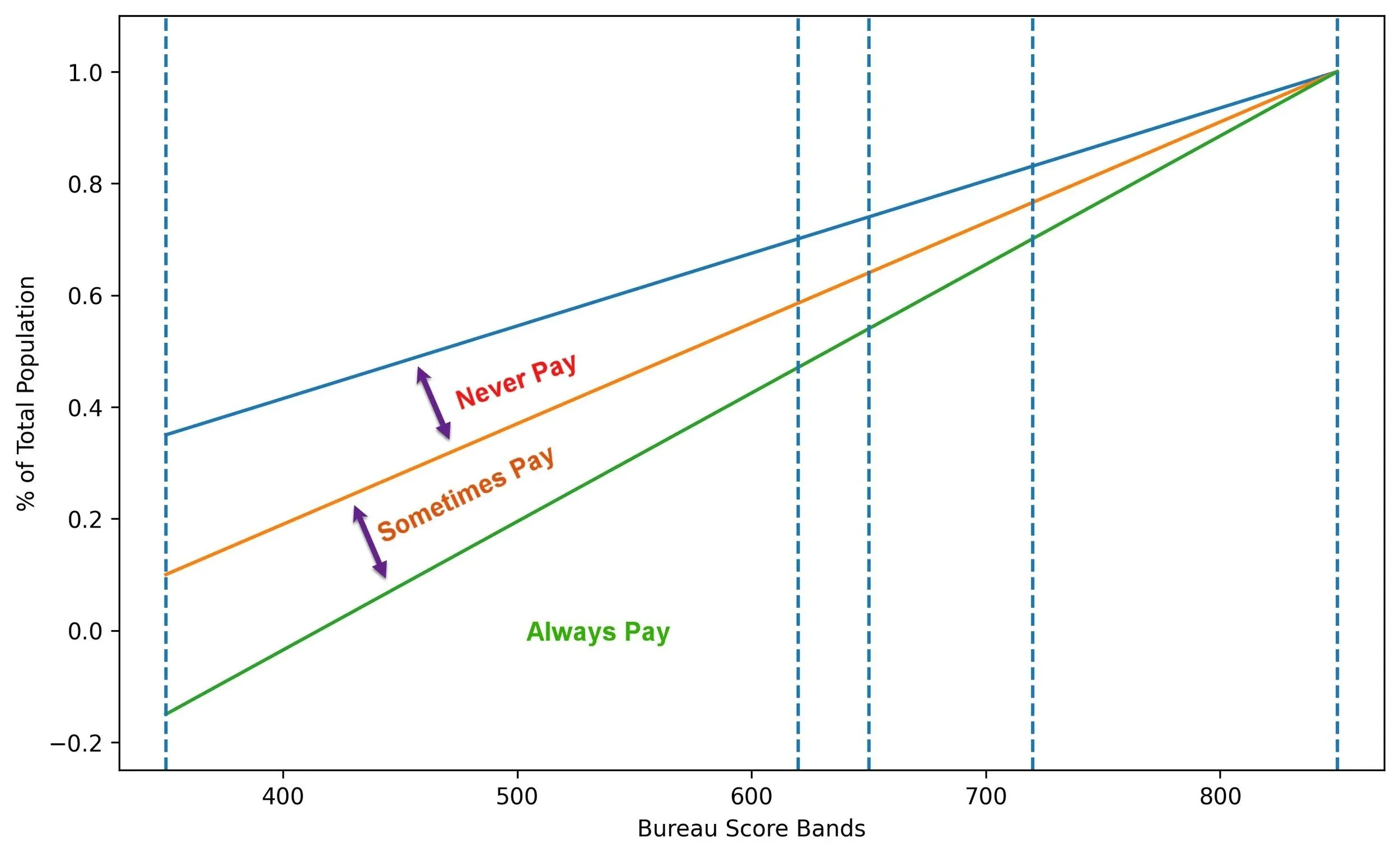

Not All Low Scores Are Equal

What if someone has a credit score under 500 — but pays every bill, on time, every time?

A new underwriting framework suggests we need to stop treating all low-score consumers the same. Instead, we should group people into three simple behavioral categories:

Always Pay – Consistently make payments, no matter their credit score.

Sometimes Pay – Make payments inconsistently.

Never Pay – Rarely or never pay back their obligations.

This model shifts the focus from the number on a credit file to the behavior behind it. By doing so, lenders can avoid wasting time and money underwriting individuals who are highly unlikely to repay, while offering fairer consideration to those who genuinely try to meet their commitments — even when life gets hard.

Spotting the Right Patterns

To make these distinctions, lenders can use specific behavioral indicators. For instance:

“Never-pay” trade lines in credit bureau data like Equifax can help flag high-risk consumers. These markers have shown to predict default with startling accuracy — over 50% default rates in many cases.

Recent payment activity — such as how many payments were made in the last three months — paints a clearer picture of intent and effort than a score alone ever could.

These aren’t just numbers. They’re signals of human behavior — of who’s trying, who’s struggling, and who’s not engaging at all.

Payment behavior varies within every score band—credit score alone does not tell the full story.

Transactional Underwriting: A Better Fit for Today

This approach fits perfectly with Congruit Credit’s mission: using real-time, behavior-based data to transform underwriting. Congruit’s tools go beyond scores, offering insight into payment patterns, ACH success rates, and income flows.

By focusing on the actual financial rhythm of consumers, lenders get:

Clearer insight into repayment risk

Smarter segmentation of applicants

Fewer charge-offs from "Never Pays"

More inclusion for the overlooked “Always Pays”

Time to Rethink What We Measure

Credit isn't just about history anymore. It’s about current behavior — and whether someone has the means and the mindset to follow through. By identifying and acting on these behavioral segments early, lenders can avoid losses, improve performance, and extend fairer access to credit.

Because sometimes, what matters most isn't what happened years ago — it's what’s happening right now.

Subscribe to Congruit for ongoing insights into how transactional data is redefining credit evaluation — and the innovations setting a new benchmark for risk assessment.

Follow us on LinkedIn